Euro vs US Dollar: Germany’s Role in Strengthening the Euro

If you’re following the ups and downs of the Euro and US Dollar, lots is happening that could impact exchange rates. Let’s break it down in simple terms.

Europe’s Economy: A Mixed Bag

The Eurozone recently reported a trade surplus of €15.5 billion, lower than last year’s numbers. Inflation is slowly cooling down, dropping from 2.5% in January to 2.4% in February, but energy prices remain high. Meanwhile, Germany—the Eurozone’s economic powerhouse—is ramping up spending on defence and infrastructure, which could push its debt-to-GDP ratio to 100% by 2034. Since Germany is borrowing more money, this can influence the entire Eurozone’s financial health.

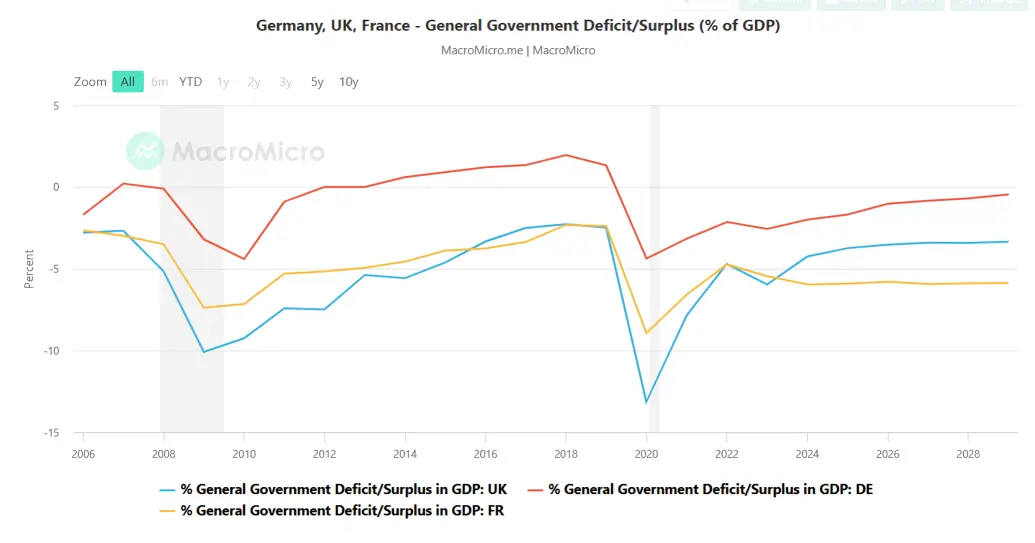

How Germany’s Fiscal Health Compares to Others in Europe

Germany clearly has the room to spend money compared to its peers.

How Interest Rates Affect the Euro

The European Central Bank (ECB) is trying to boost the economy by cutting interest rates. They have reduced:

Deposit rate to 2.50%

Main refinancing rate to 2.65%

Marginal lending rate to 2.90%

Lower interest rates can make borrowing cheaper, encouraging spending and investment, which could boost the Euro in the medium term.

Why the Euro Could Strengthen

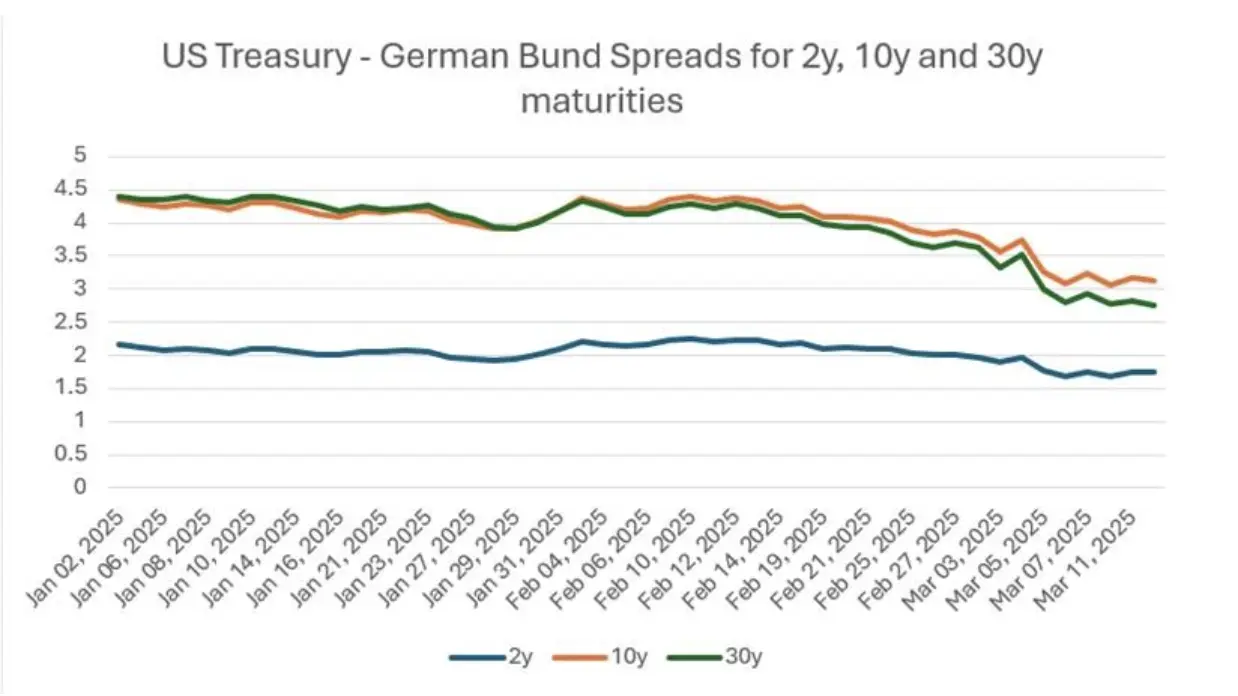

Bond Markets are Shifting: The gap between US Treasury and German Bund yields is narrowing. In simple terms, investors may start favouring the Euro over the Dollar when European yields go up.

Government Spending: With Germany increasing its spending, other European countries might follow suit. This could stimulate the economy and push the Euro higher.

Rate Cuts Could Help: Lower interest rates generally support economic growth, strengthening the Euro over time despite short-term outflows.

What Could Hold the Euro Back?

Tariff Wars: Trade tensions between the US and EU could hurt exports, making it harder for the Euro to gain momentum.

Debt Concerns: Many Eurozone countries are already deep in debt. Without Germany’s help, they might struggle to keep up.

US Interest Rates: The US Federal Reserve (led by Jerome Powell) isn’t backing down on fighting inflation. If they keep interest rates high, the US Dollar could remain strong.

Bottom Line

The Euro is at an interesting crossroads. While economic stimulus and government spending could help it gain ground, uncertainty around trade, debt, and US interest rates could limit its rise. If you’re monitoring exchange rates, pay close attention to how Germany’s spending plans unfold and how the US responds to inflation in the coming weeks.

Stay tuned for more updates as we track these market trends!

Trump 2.0: Major Policy Overhaul Reshapes US Markets

On January 20, 2025, as Donald Trump embarked on his second term, he unleashed a torrent of executive orders, signalling a dramatic policy shift across various sectors, which traders and investors should closely monitor for market implications.

Immigration and Border Security

National Emergency Declaration: Trump declared a national emergency at the US-Mexico border, authorising the deployment of military forces, including the National Guard, to bolster border security. This move is anticipated to ramp up spending on defence and security contractors.

Border Wall Continuation: With the resumption of border wall construction, companies in construction, security technology, and infrastructure could see a surge in demand.

Immigration Policy Overhaul

Ending Birthright Citizenship: A policy aimed at reducing incentives for illegal immigration, potentially affecting labour markets in sectors like agriculture and service industries.

Refugee Program Suspension: A six-month pause on refugee admissions could influence sectors dealing with international aid and resettlement services.

Asylum Policy Changes: The “Remain in Mexico” policy’s revival will increase demand for border management services and could lead to legal challenges, affecting market stability.

Deportation Initiatives: With enhanced deportation measures, private prison companies might see growth, while labour markets face potential disruptions.

Cartel Designation: Labelling certain cartels as terrorist organisations could lead to heightened security measures, impacting trade routes and logistics firms.

Economic and Trade Measures

TikTok Policy Review: The 75-day extension on the TikTok ban could sway investor sentiment in the tech sector, particularly for companies with ties to ByteDance or similar entities.

Tariff Proposals: Plans for up to 25% tariffs on Canadian and Mexican goods could reshape trade dynamics, affecting industries reliant on cross-border trade.

External Revenue Service: Aiming to improve customs duty collection, this could introduce new administrative burdens or opportunities for logistics and customs consulting firms.

Inflation Combat Measures: Emergency consumer relief could signal increased government spending, impacting bond markets and currency values.

Trade Review: A reassessment of trade with major partners like China, Canada, and Mexico might result in volatility in sectors sensitive to trade policies.

Energy and Climate Policy

Paris Agreement Withdrawal: This signals a US pivot back to fossil fuels, potentially boosting oil and gas sectors while challenging renewable energy investments.

Offshore Drilling Expansion: Opening new areas for drilling could benefit oil exploration companies but face environmental and legal pushback.

Strategic Petroleum Reserve: Plans to refill could influence oil prices globally.

Regulatory Rollbacks: Cancelling efficiency standards on appliances and reversing EV mandates could tilt the market towards traditional energy companies while reducing demand for green tech.

Wind Farm Leasing Cancellation: This will likely impact renewable energy developers but could spur interest in alternative energy investments.

Federal Workforce and Government Operations

Return-to-Office Mandate: This could stimulate demand for office space and services but might also challenge federal workers’ unions.

Hiring Freeze: Exceptions for critical roles suggest continued investment in defence and security, potentially benefiting related industries.

Regulatory Review: Suspended new regulations could provide short-term relief for businesses but create uncertainty.

DEI Initiative Termination: This could affect diversity consulting and training sectors, signalling a shift in corporate culture expectations.

Healthcare and International Relations

WHO Withdrawal: This could affect global health policy and international operations in pharmaceutical sectors.

Military Vaccine Mandate Reversal: This might influence health sector stocks, particularly those involved in vaccine production.

Cultural and Social Policy

Gender Policy: A two-gender policy might lead to legal battles and social unrest, influencing sectors from education to healthcare.

DEI Program Cuts: This could shift the focus of educational institutions and corporations towards different priorities.

The sweeping policy changes on President Trump’s first day in office mark a decisive shift in the US political and economic landscape. Immigration, energy, and trade policies are key focus areas, with ripple effects across multiple industries. While traditional energy and defence sectors could benefit from the administration’s immediate actions, technology and renewable energy may face challenges. These changes, coupled with potential trade tensions and regulatory rollbacks, create a dynamic environment for investors and businesses. Monitoring these developments will be crucial as markets adjust to this strategic overhaul.

Sector-Specific Reactions

Technology: Despite initial gains, tech stocks, especially those with significant international exposure or reliance on global supply chains, faced uncertainty due to potential tariff implications.

Energy: Traditional energy stocks might have seen an uptick with the policy shift towards fossil fuels, although immediate market reactions might have been tempered by broader market concerns.

Defence and Security: Companies in these sectors could have seen positive movements due to increased border security measures.

Currency and Bonds: The US dollar strengthened against some currencies, particularly in response to potential trade policies, while bond yields showed mixed outcomes, with some suggesting that high valuations could lead to corrections if inflation accelerates due to new tariffs.

Technical Analysis

S&P 500

Outlook: Bullish

NASDAQ

Outlook: Bullish

Image Source: TradingView | For Illustrative Purposes Only

Strong Jobs Report, Rising Yields, and Market Volatility

The recent US employment report highlighted an unexpectedly robust labour market, with 256,000 new non-farm jobs added, surpassing the anticipated 165,000. The unemployment rate declined to 4.1%, better than the expected 4.2%, while the labour force participation rate remained steady at 62.5%.

Wage growth, a key metric for inflation, also came in as expected. Average hourly earnings rose by 0.3% month-over-month and 3.9% year-over-year, slightly below the anticipated 4%. This suggests that wage-driven inflation isn’t spiralling out of control, which relieves policymakers.

When Good News Triggers Market Uncertainty

At first glance, strong job numbers and a robust economy seem like positive developments. However, this phenomenon, often referred to as “Good News for Economy is Bad News for Stocks” in financial terms, happens when strong economic data unexpectedly leads to market declines.

The Fed’s Dilemma: A strong economy means the Fed has less pressure to cut interest rates. Higher interest rates are typically used to cool down an overheating economy, but they also increase borrowing costs for businesses and consumers. Given the current strength of the job market, the Fed is likely to hold off on rate cuts—something the market had been anticipating, with expectations now pointing to no rate cuts until at least October this year.

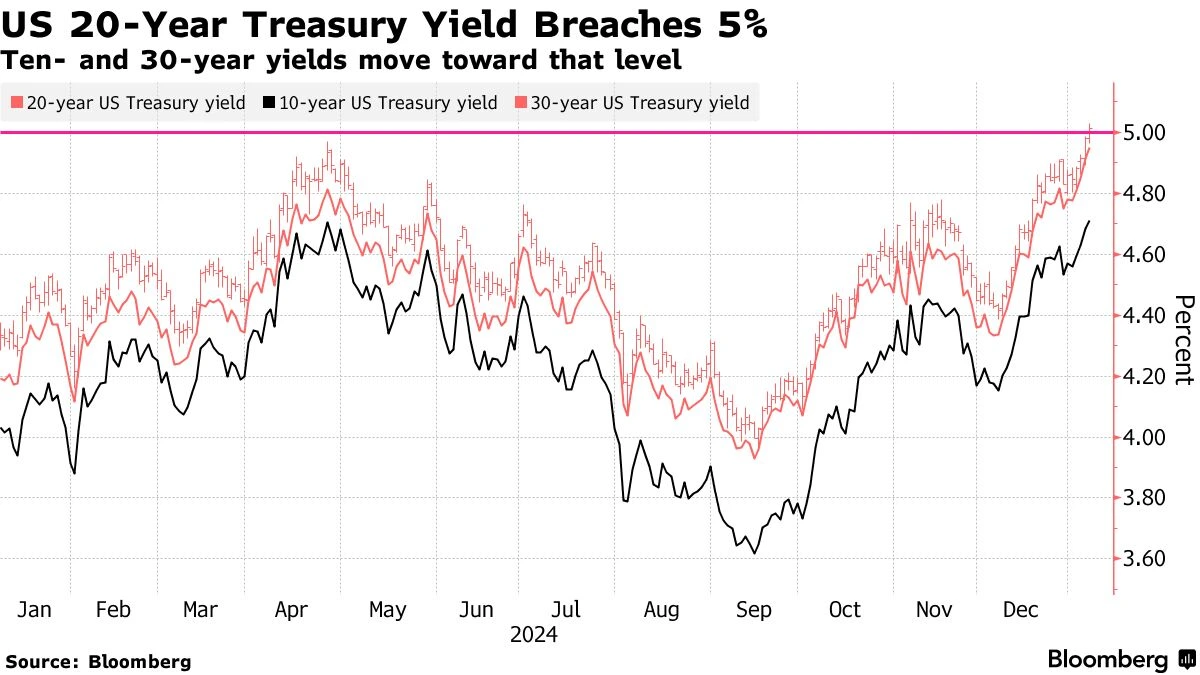

Bond Yields Rise: When the Fed signals that it won’t cut rates soon, bond yields tend to rise. This happens because higher interest rates make existing bonds less attractive, causing their yields to climb. The 10-year treasury yield, a key benchmark for borrowing costs, has recently risen and is now approaching 5%. This surge reflects shifts in economic conditions and monetary policy, driven by concerns over inflation and escalating government debt. If this trend persists, it could materially shift the investment landscape, catching many investors off guard.

Stock Market Pressure: Higher yields mean higher borrowing costs for companies, particularly smaller firms that rely heavily on debt. This often weighs on stock markets, especially small-cap indices like the Russell 2000. In short, good economic news can lead to market sell-offs as investors recalibrate their expectations for rate cuts.

What Lies Ahead? Key Trends to Watch

As the financial landscape evolves, several factors will shape the markets in the coming months:

Bond Yields: How High Can They Go?

The recent surge in bond yields has left investors wondering just how much higher they can climb. The 20-year treasury yield recently broke past 5%, a level not seen since 2023, while the 10-year and 30-year yields are inching closer to their 2023 peaks. This upward trend is being driven by fears of inflation, concerns over widening deficits, and the resilience of the US economy.

Yields have been on the rise since the Fed began its rate-cutting cycle in September. The combination of a strong economy and President-elect Donald Trump’s victory has only accelerated this trend, pushing the 10-year yield more than 100 basis points higher than before the Fed’s first cut.

While there may still be room for yields to rise, historical patterns and strong demand for safe-haven assets like treasuries could limit their ascent. The Federal Reserve’s next moves will be critical—any signals of rate hikes could push yields even higher, while a dovish pivot might help stabilise them.

The US Dollar’s Strength: A Two-Sided Coin

A strong US economy and rising bond yields typically boost the US dollar, but this strength comes with trade-offs. A stronger dollar makes American exports more expensive, potentially hurting US companies that rely on global markets. It also tends to draw capital away from emerging markets, as investors chase higher returns in the US. Additionally, a robust dollar often puts downward pressure on commodity prices, including gold, which could face further challenges.

Global Ripples: Japan in the Spotlight

The impact of a stronger dollar and higher US yields extends far beyond American borders. One economy to watch closely is Japan. A weaker yen, driven by a stronger dollar, could push inflation higher in Japan, potentially forcing the Bank of Japan to raise interest rates sooner than expected. This would mark a significant shift in Japan’s monetary policy, with ripple effects across global markets.

Beyond the Short-Term Noise

While the immediate reaction to strong job data might trigger a market sell-off, there’s a positive side to this story. A robust economy lays the foundation for stronger corporate earnings, which are the ultimate driver of stock prices over the long term. Yes, the market may see fluctuations in the short term as investors adjust to delayed rate cuts, but for those who believe in the resilience of the US economy, the long-term outlook remains promising. For long-term investors, this could even be an opportunity to buy at lower prices. While markets may fluctuate, economic strength tends to win out in the long run.

Trumpian Resurgence and Its Global Implications: An Outlook for 2025

The year 2025 stands on the horizon as a pivotal moment, shaped by Donald J. Trump’s return to the White House on Monday, January 20, 2025. His influence, both actual and expected, has a major impact on the global economy and politics. The prospect of a second Trump presidency brings a mix of optimism for domestic growth and apprehension about global instability, creating a complex set of opportunities and risks.

A Trump presidency in 2025 is expected to reignite the pro-business policies that defined his first term. Tax cuts, deregulation, and a focus on domestic manufacturing could significantly boost the US economy. Sectors like technology, energy, and infrastructure are likely to thrive. This optimism is rooted in the belief that Trump’s policies will create a favourable environment for corporate profitability and economic expansion.

Lessons from the 2017 Tax Cuts

The 2017 Tax Cuts and Jobs Act (TCJA) offers a glimpse into what 2025 might hold. The tax cuts initially boosted GDP growth to 2.9% in 2018 and propelled corporate profits, with S&P 500 earnings surging by 20% that year. However, the long-term economic impact was limited, as growth slowed to 2.3% by 2019, and much of the tax savings were funnelled into stock buybacks rather than productive investments. As Trump returns to office in 2025, similar policies could provide a short-term economic boost but may struggle to deliver sustained growth without addressing underlying structural challenges.

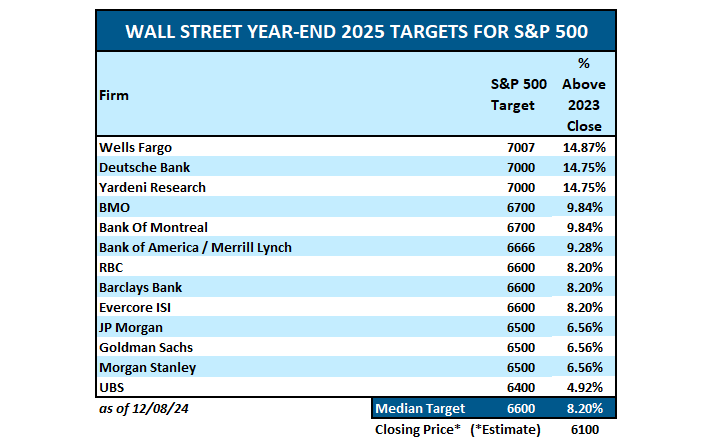

Stock Market Forecast for 2025

Image Source: Investing.com

Market forecasters are optimistic about a broad-based rally in 2025, driven by Trump’s pro-business agenda. Following his re-election in November 2024, the Dow Jones Industrial Average, S&P 500, and Nasdaq surged, reflecting investor enthusiasm. The S&P 500 is predicted to reach 7,000 points, while the Dow Jones is expected to follow a similar trajectory, with potential gains of 8-12%, driven by strong performance in industrials, energy, and financial sectors.

The Nasdaq, which rose nearly 29% in 2024, is expected to remain a strong performer, particularly in technology and AI-driven sectors. Forecasts suggest the Nasdaq could climb by 10-15%, fuelled by continued innovation in artificial intelligence, semiconductor technology, and biotech. However, some caution remains, as Trump’s proposed tariffs and immigration policies could introduce volatility, particularly for tech companies reliant on global supply chains.

Inflation and Monetary Policy

Inflation remains a critical concern as the year progresses. Trump’s focus on tariffs and immigration restrictions will likely exert upward pressure on prices, complicating the Federal Reserve’s efforts to maintain stability. Core inflation in the US could hover around 2.5%, above the Fed’s target, potentially limiting the central bank’s ability to cut interest rates as aggressively as markets hope. This delicate balancing act between growth and inflation will the year’s defining feature.

Globally, central banks face similar challenges. The ECB and the BoE are expected to cut rates more aggressively than the Fed, which could lead to a stronger US dollar. While a strong dollar benefits American consumers, it could weigh heavily on emerging markets, exacerbating global trade imbalances and financial instability. The interplay between Trump’s policies and central bank actions will be a key theme, with any missteps likely to trigger market turbulence.

Geopolitical Risks

Beyond economics, the geopolitical implications of a Trump presidency are profound. His “America First” stance could lead to a more isolationist US foreign policy, potentially weakening alliances and creating power vacuums in regions like Europe and Asia. The ongoing tensions between the US and China could escalate, particularly if Trump follows through on his campaign promises to impose up to 60% tariffs on Chinese imports and 10-20% on goods from other countries. Such measures could trigger retaliatory actions, leading to a global trade war and disrupting supply chains worldwide.

Trump’s unpredictable style adds another layer of complexity. His willingness to challenge international norms and institutions could create a more fragmented and volatile global order. This unpredictability makes it difficult for investors and policymakers to predict the future, increasing the importance of resilience and adaptability in navigating the year ahead.

High Stakes & Strategic Navigation

2025 promises to be a year of high stakes, with Trump’s potential return serving as the central narrative. While his policies could drive economic growth and market optimism in the US, the risks of trade wars, inflation, and geopolitical instability loom large. The global economy will need to navigate this uncertainty with care, focusing on resilient sectors and diversified strategies to mitigate risks. As the world prepares for a potential Trumpian resurgence, the only certainty is that 2025 will be a year of profound transformation, demanding both caution and strategic creativity to navigate effectively.

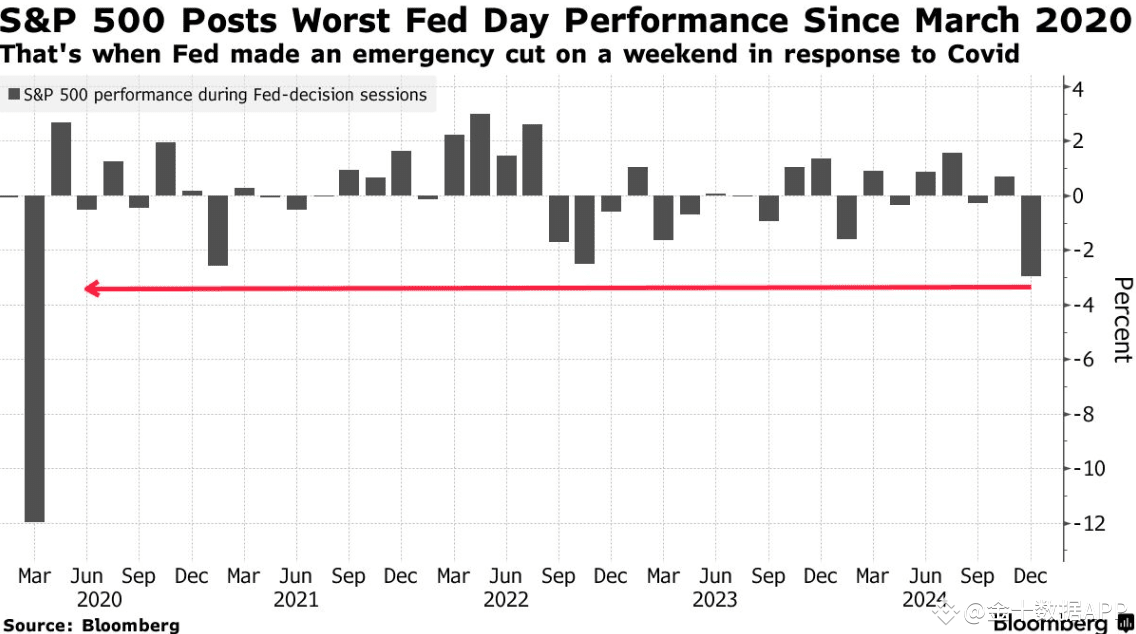

Fed Signals Slower Rate Cut Path Despite Third Consecutive Reduction

The Federal Reserve delivered its third consecutive rate cut yesterday, bringing the federal funds rate to 4.25%-4.50% while signalling a more cautious approach to future easing. In their latest quarterly projections (Dot Plot), Fed officials significantly scaled back their rate cut expectations for 2025. The median forecast shows only two 25-basis-point reductions next year, down from previous estimates, bringing rates to 3.75%-4% by year-end. This contrasts with most economists surveyed by Bloomberg, who anticipate three cuts in 2025.

Fed Chair Jerome Powell emphasised that with cumulative cuts now totalling 100 basis points from the peak, the stance of monetary policy has meaningfully eased. “We can therefore proceed carefully as we consider further adjustments to our policy rate,” Powell stated during the post-meeting press conference. He maintained that while the policy remains restrictive, the Fed is “still on a path to cut rates”.

The updated economic projections revealed heightened concerns, with officials raising their end-2025 inflation forecast to 2.5% from 2.1% in September. The unemployment rate is expected to settle at 4.3% next year, while GDP growth forecasts were slightly upgraded to 2.1%.

Looking ahead, Powell addressed questions about potential Trump administration trade policies, noting that while some policymakers have begun incorporating possible effects of higher tariffs into their forecasts, the impact remains highly uncertain. “We don’t know much about the actual policies,” Powell marked, suggesting it was premature to conclude.

Markets responded negatively to the Fed’s more hawkish tone, with the S&P 500 experiencing its worst decline since January, dropping 2%. Treasury yields reflected the shift in rate expectations, with the 2-year yield jumping 11 basis points to 4.35%, while the dollar strengthened against major currencies. While the market initially reacted negatively to the Fed’s hawkish tone, a closer look suggests this reaction may have been exaggerated.

Powell’s commentary revealed a shift in the Fed’s risk assessment. This shift showcases increased concern about inflation persistence while expressing less worry about labour market conditions. This perspective reflects the underlying strength of the US economy, which gives the Fed more room for careful policy adjustment.

Economic Projections Show Strength Amid Inflation Concerns

A careful examination of the Fed’s economic projections tells a nuanced story. While inflation forecasts for 2025 were revised upwards, GDP growth projections also saw an upgrade, suggesting a robust economic outlook. The dot plot now indicates two rate cuts in 2025 instead of four, but the total projected cuts through 2027 decreased only by one, from six to five.

Powell’s communication style remained consistent with previous meetings, maintaining a cautious tone while softening some of the dovish language, without shifting towards a more aggressive stance. The reduction in projected rate cuts appears more like a timing adjustment than a fundamental change in policy direction.

A strategic perspective suggests that the market’s sharp reaction may present buying opportunities in US equities once volatility settles, potentially within the next few days to a week.

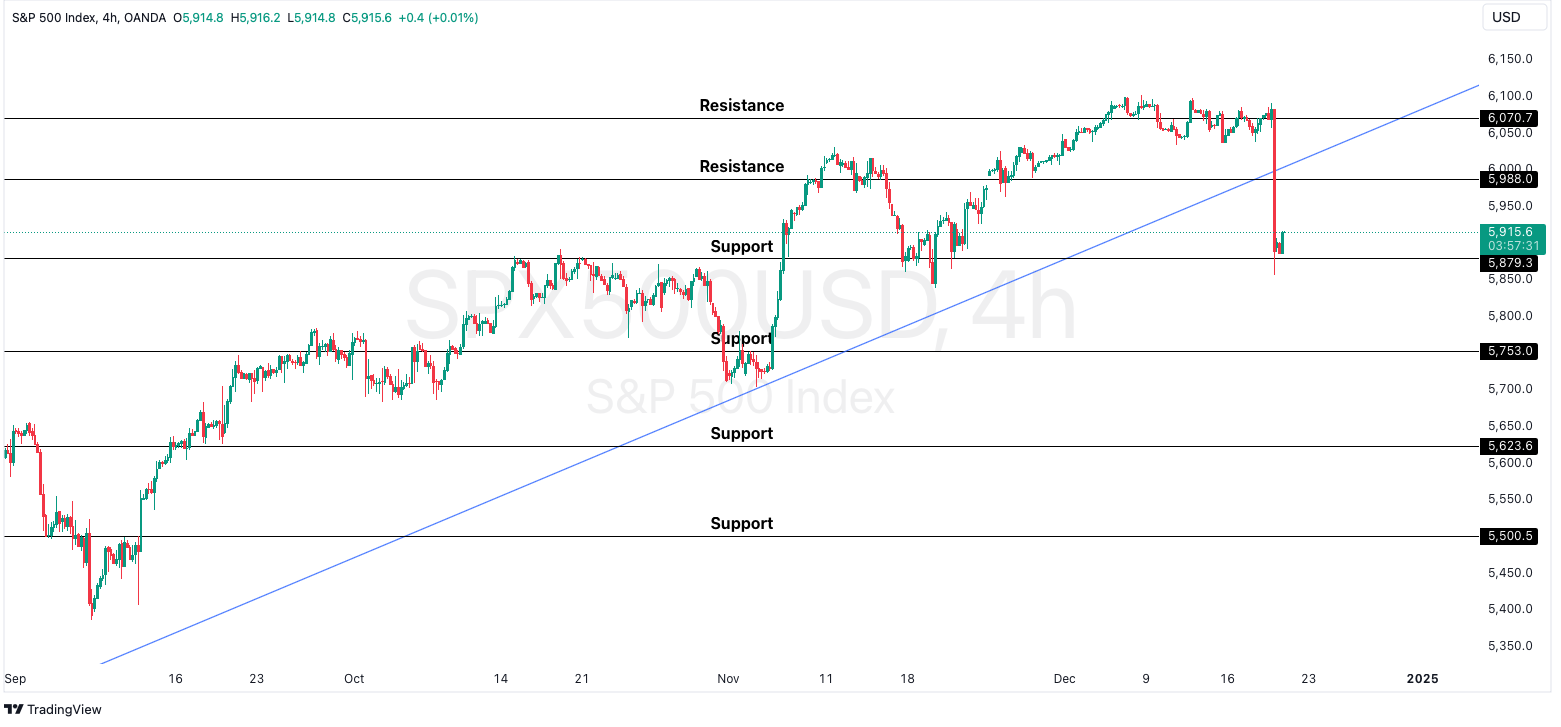

Technical Analysis

S&P 500

Image Source: TradingView

From a technical analysis standpoint, the S&P 500 is currently testing its support level ($5,879). Should this level hold, it would suggest that the market isn’t overreacting to the recent Fed rate cut, signalling stability despite the hawkish tone in the central bank’s outlook. A recovery from this support could pave the way for a potential rally back to all-time highs.

However, there is also the possibility that the S&P 500 could dip further to test a deeper support level of around $5,500. This could be a strategic move to capture liquidity before the market sets up for its next upward trend. Monitoring the market’s response to the Fed’s policy outlook is crucial, as it will provide insights into whether the market can sustain a recovery or if a deeper correction is necessary for a more stable rally.

FOMC Meeting: Inflation Signals Rate Cut, But Caution Looms in 2025

The Federal Open Market Committee (FOMC) meeting on Wednesday, December 18, is expected to be a key event this week, with a widely anticipated 25-basis point interest rate cut. Recent economic indicators, including the November jobs report and inflation data, suggest the Fed is navigating a shifting economic landscape. With inflation showing signs of moderation and the economy facing potential headwinds, this rate adjustment reflects the Fed’s ongoing effort to balance growth and manage inflationary pressures.

Last week’s inflation numbers have influenced this rate change, with both the CPI and the PPI meeting expectations and showing no significant surprises. Additionally, a slight uptick in unemployment has reinforced the view that the labour market is no longer an important driver of inflation. With the Fed already projecting two rate cuts in 2024, one of which was implemented in November, the market is now pricing in a 95% likelihood of another 25-basis point reduction in December, likely concluding the Fed’s easing cycle for the year.

2025: A Shift Towards Caution and Measured Easing

While December’s rate cut seems almost certain, the path ahead in 2025 is clouded with uncertainty. Inflation has cooled, but progress has slowed in recent months, making the disinflation trajectory harder to predict. Adding to this uncertainty are potential shifts in fiscal, trade, and immigration policies, which could complicate the Fed’s efforts to reach a neutral interest rate—a level that neither stimulates nor restricts economic activity.

Considering these complexities, the Fed’s updated December dot plot is expected to signal a more cautious approach to future rate cuts. Analysts are forecasting 2-3 cuts in 2025, with the federal funds rate potentially settling in the 3.5% to 4% range by the end of the year.

A Delicate Balance for the Road Ahead

As the Federal Reserve faces these challenges, its monetary policy decisions will be closely watched. The market will pay close attention to external factors—such as fiscal policy changes and global trade dynamics—that could influence the Fed’s approach. The coming year will likely see a more measured, cautious stance as the Fed seeks to support sustainable growth while avoiding inflationary pressures.

Global Central Banks Move Towards a Neutral Policy Stance

The trend towards neutral monetary policy is not confined to the US. Other central banks are also adjusting their rates to strike a similar balance. The BOC made a bold move last week, cutting its policy rate by 0.5% to 3.25%, now at the top of its neutral range. This follows a swift 1.75% rate reduction over the past six months, the fastest pace among advanced economies.

Meanwhile, the ECB lowered its rates by 0.25%, bringing the policy rate to 3%, while Switzerland’s central bank surprised markets with a 0.5% reduction—the largest in nearly a decade. This week, all eyes will be on the FOMC meeting on Wednesday, December 18, while the BOE and BOJ are also in focus, with both expected to hold rates steady on Thursday, December 19.

Technical Analysis

GBP/USD

Image Source: TradingView

From a technical standpoint, GBP/USD is experiencing a strong bearish trend on the daily timeframe. In the near term, it is advisable to consider short positions around the resistance level, as the prevailing market sentiment favours further downside movement. However, for those looking to enter long positions, the safer entry point would be at the support level of $1.21677. This level may offer a more favourable risk-to-reward ratio should the price test and hold this area.

USD/JPY

Image Source: TradingView

From a technical perspective, USD/JPY will likely trade within a consolidative range this week as the market awaits key news from the BOJ and the Fed. A move towards the resistance level at ¥154.858 is possible, but a corrective pullback is expected afterwards.

The prevailing market bias remains tilted towards short positions in the near term, with the potential for a move down. Should the price test and hold this level, a buying opportunity could arise around the support zone at ¥150.694. A decisive break below ¥150.694 would signal a shift in market sentiment, increasing the likelihood of further downside and potentially targeting the next support at ¥144.5.

Top Financial Market Risks for 2025

In 2021, the global economy started recovering from the pandemic recession. However, a few global financial market risks remain.

Key Takeaways

The financial markets are recovering from the coronavirus recession, although many risks remain.

The main financial market risks are inflation, geopolitical conflicts, and uncertain election results.

Central banks have lowered interest rates as inflation eases, with both US Federal Reserve and Bank of England cutting rates in recent months.

Top Financial Market Risks for 2025

The financial markets in 2025 have been beset with various risks, including inflation, geopolitical tensions, and a slew of elections. Below, we will discuss the different types of risks in financial markets and possible ways investors can address them.

Inflation Rate to Spike Again

Inflation in the US has fallen to 2.4%, gradually approaching the 2% target, while in the UK it has fallen to 1.7%, below 2% for the first time in over three years. Despite inflation having eased since the pandemic-led volatility, the risk of a resurgence in the near future remains. However, the International Monetary Fund (IMF) warned of rising financial market risks even though “the global battle against inflation has largely been won”. The central banks need to be vigilant to further bring an end to inflation, the Fund noted.

However, the risk of rising inflation, particularly among low-income countries, remains. Inflation is another financial market risk that could again threaten global economy. Central banks have lowered interest rates as inflation eases, with the US Federal Reserve and Bank of England cutting rates in recent months. However, a renewed spike in inflation could prompt more rate hikes, impacting economic growth and investor activity.

Market Volatility

Volatility measures the extent to which an asset’s price deviates from its average. High volatility leads to wider price ranges and sudden price swings, creating turbulence in the market.

Thus, the general public is not left with disposable funds to enthusiastically participate in markets. Such a situation is very volatile, and risk sharing in financial markets, i.e., risks are proportionally distributed amongst all the participants, can address it.

The Potential Decline of Overvalued Tech Companies

The rapid rise of tech stocks has driven strong equity market returns thanks to the AI boom and transformative tools like OpenAI’s ChatGPT. Leading tech companies—Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla—have all demonstrated extraordinary growth due to the adoption of AI technology. This has led to a high concentration of the tech sector in the equity market. Many experts reasonably wonder whether the hype around AI justifies—or inflates—tech company valuations. When Nvidia reported its financial results for Q2 2024 in late August, the market was hardly impressed with the company’s revenue estimate of $32.5 billion for the next quarter. The company’s stock fell around 9% following the result.

Many tech companies have been unable to leverage AI to significantly increase their revenues. If the tech companies are overvalued, it could indeed be a case of a tech bubble that could potentially burst. A potential tech bubble burst would pose a terrible risk to the entire market, as the sector has become dominant. Traders need to keep a close watch.

Election Surprises

In 2024, 40 countries accounting for 42% of global GDP will hold elections, including three of the five largest economies: the US, Japan, and India.

United States: The US Presidential election will be held in early November. The incumbent Democratic Party, led by Kamala Harris, will be challenged by the Republican Party, led by Donald Trump. Inflation and immigration are the most important issues for voters. Depending on the election results, it could shift subsequent economic policy in the world’s largest economy.

Japan:The general election in Japan will be held towards late October, with the main opposition party, the Constitutional Democratic Party of Japan (CDPJ), set to challenge the ruling Liberal Democratic Party (LDP). Inflation and corruption are some of the key concerns for voters.

India: Under the leadership of Prime Minister Narendra Modi, the right-wing Bharatiya Janata Party (BJP) managed to score its third victory in a row. However, the party lost its majority in this election. Though the country’s economy became the fifth largest in the world under Modi’s tenure, the issues of inflation, unemployment, and income inequality continue to tag along.

United Kingdom: In the UK, the incumbent Conservative Party, led by Prime Minister Rishi Sunak, lost the election to the Labour Party led by Keir Starmer. Experts attribute the loss of Conservatives to their poor performance on key economic issues such as inflation, cost of living, healthcare, housing, and education. Most experts do not anticipate any major re-evaluation of any country’s current economic policy, regardless of the election results. But we should always be ready for unpredictable decisions.

Bottom Line

If these financial market risks could be addressed successfully, markets could improve further. However, concerns remain that inflation, volatility, and election effects will prevent them from returning to pre-pandemic levels.

The only way forward is for investors to be prepared beforehand with a detailed plan to deal with market risks. One strategy is to leverage risk management practices. Depending on how the situation is handled, we can anticipate steady market growth for the next few months. For that to happen, regulatory bodies, asset issuers, trading exchanges, and institutional and retail investors must demonstrate resilience and be willing to cooperate.